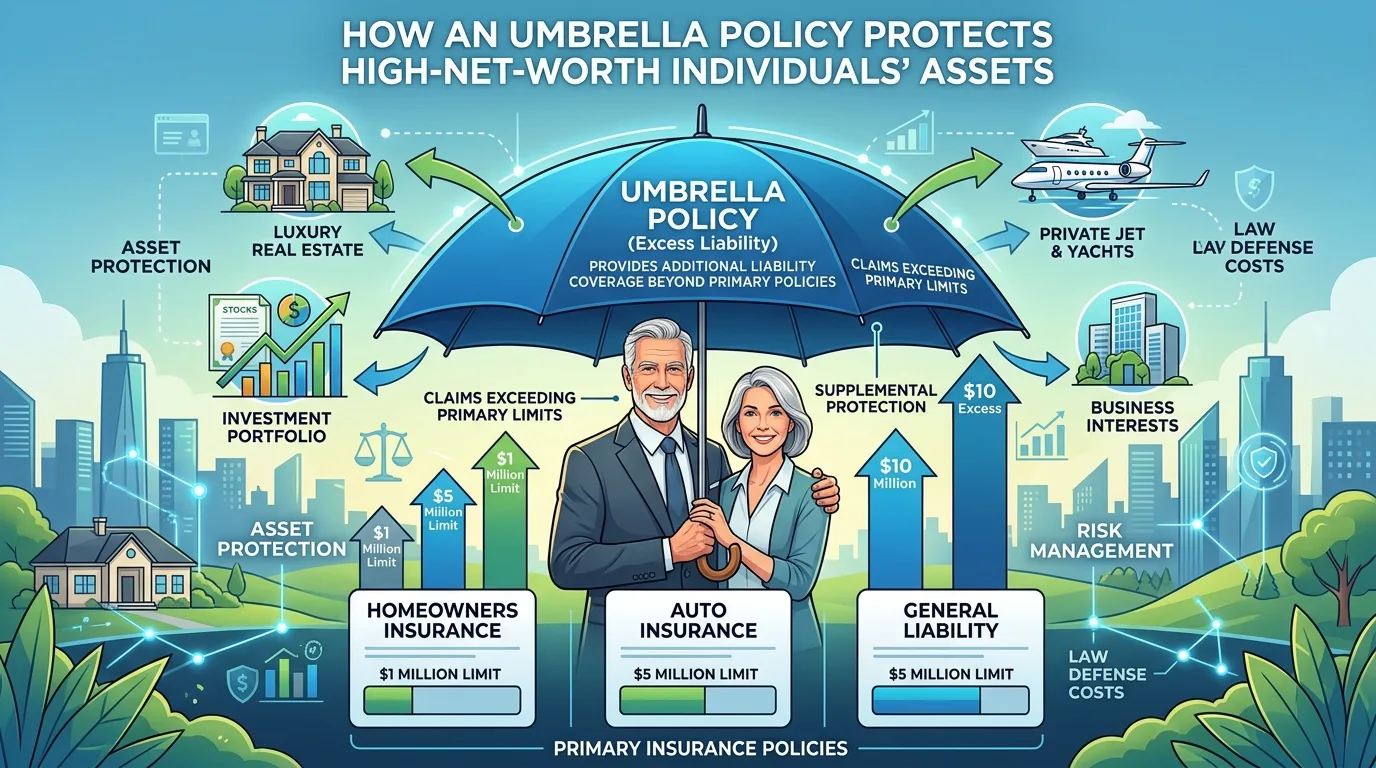

As a high-net-worth individual, you've worked hard to accumulate wealth and assets. But with great wealth comes great responsibility – particularly when it comes to protecting your financial future from unexpected events. One critical component of a well-rounded insurance strategy is the umbrella policy, designed to shield your assets from liability risks that could deplete your wealth. In this article, we'll delve into the world of umbrella policies, exploring their unique features, benefits, and how they can help fill gaps in your existing coverage.

What is an Umbrella Policy?

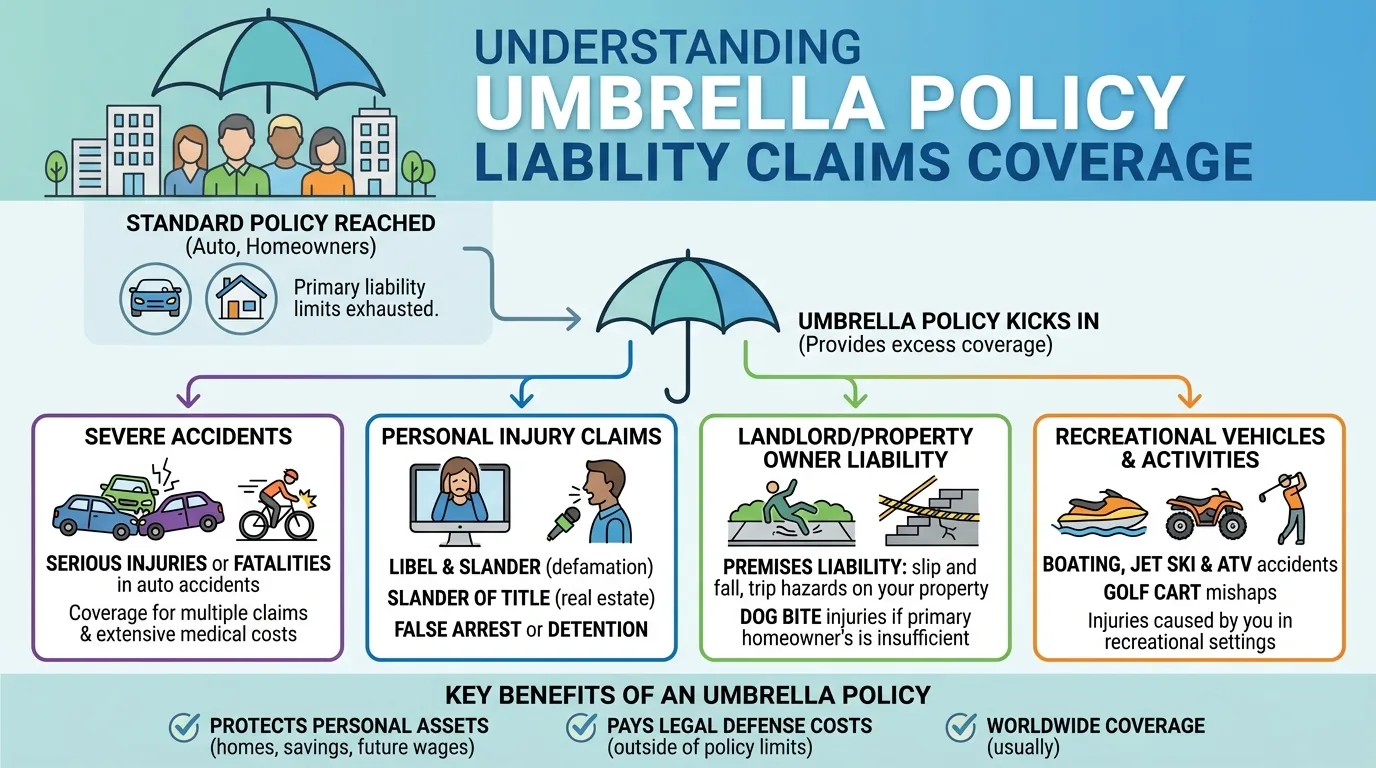

An umbrella policy is a type of liability insurance that supplements your primary insurance policies, such as home, auto, or boat insurance. Its primary purpose is to provide additional financial protection against lawsuits, judgments, or settlements related to accidents or other incidents where you may be held liable. Think of it like a safety net: if you're involved in an incident and the damages exceed the limits of your primary policies, your umbrella policy kicks in to cover the remaining amount.

To understand how umbrella policies work, let's break down the concept of liability insurance:

Liability insurance is designed to protect against claims made by others for injuries or property damage.

Primary insurance policies typically have specific coverage limits, which may not be sufficient to cover catastrophic events.

Umbrella policies provide additional protection beyond these primary policy limits.

How Does It Differ from Regular Insurance?

Umbrella policies are distinct from regular insurance for several reasons:

Higher coverage limits: Umbrella policies offer significantly higher coverage limits than standard insurance policies. This means that even if you're involved in a catastrophic event, your umbrella policy will help ensure that your assets remain protected.

+ For example, a primary auto insurance policy may have a limit of $300,000 per incident. However, an umbrella policy can provide additional coverage up to $1 million or more, depending on the policy and provider.

Broader liability protection: While primary policies typically cover specific risks (e.g., auto accidents or property damage), umbrella policies provide more comprehensive protection against a wide range of liability claims.

+ Umbrella policies may cover employment-related liabilities, defamation or libel claims, and other types of lawsuits that could deplete your assets.

Lower premiums: Despite offering higher coverage limits and broader protection, umbrella policies often come with lower premium costs compared to purchasing separate insurance policies for each risk.

Key Features and Benefits of Umbrella Policies

Here are some essential features and benefits of umbrella policies:

Supplemental coverage: Umbrella policies cover excess liability not covered by your primary insurance policies.

Multi-risk protection: They provide comprehensive protection against a range of risks, including:

+ Accidents or injuries caused to others + Property damage or theft + Defamation or libel claims + Employment-related liabilities (e.g., employee lawsuits)

Increased asset protection: By shielding your assets from liability risks, umbrella policies help safeguard your net worth.

+ For example, if you're sued for $500,000 and your primary policies have limits of $300,000, an umbrella policy can provide the additional coverage needed to protect your assets.

Customizable coverage: Many insurers offer flexible policy options to accommodate individual needs and circumstances.

How to Choose the Right Umbrella Policy

To select an effective umbrella policy, consider the following factors:

1. Assess your financial situation: Evaluate your net worth, income, and assets to determine how much liability protection you need. + Consider your overall financial picture, including any debts, investments, or business interests that could impact your insurance needs. 2. Review existing insurance policies: Ensure that your primary policies have sufficient coverage limits to prevent gaps in your overall protection. + Check the coverage limits of each policy and ensure they align with your individual circumstances. 3. Research insurers and options: Compare policy features, premium costs, and reputation among top insurers.

When selecting an umbrella policy, it's essential to carefully review the terms and conditions, including:

Coverage limits

Policy exclusions

Premium costs

Deductibles

Filling Gaps in Your Existing Coverage

While umbrella policies are an essential component of a comprehensive insurance strategy, it's equally important to identify areas where existing policies may be lacking. Consider the following potential gaps:

Under-insured primary policies: If your primary policies have inadequate coverage limits or insufficient protection against specific risks.

+ For example, if you own multiple homes or businesses, ensure that each policy has sufficient coverage limits and comprehensive protection.

Uninsured assets: Assets not covered by your primary policies (e.g., a vacation home or investment properties).

+ Consider purchasing separate insurance policies for these assets to fill the gap in coverage.

Employment-related liabilities: If you're self-employed or own a business, consider an umbrella policy that covers employment-related liabilities.

Case Study: The Importance of Umbrella Policies

Consider the following scenario:

John is a successful entrepreneur with a net worth of $5 million. He owns multiple businesses and has primary insurance policies to cover his assets. However, one day, he's sued for $1.5 million due to an employment-related lawsuit. His primary policies have limits of $300,000 per incident, leaving him exposed to the remaining amount.

In this case, a comprehensive umbrella policy could provide the additional coverage needed to protect John's assets. An effective umbrella policy would:

Cover excess liability beyond primary policy limits

Provide multi-risk protection against employment-related liabilities and other risks

Offer customizable coverage options to accommodate individual needs

Conclusion

Umbrella policies are an essential component of a comprehensive insurance strategy for high-net-worth individuals. They provide additional financial protection against liability risks, ensuring that your assets remain safeguarded in the event of catastrophic events.

When selecting an umbrella policy, carefully review the terms and conditions, including coverage limits, policy exclusions, premium costs, and deductibles. Consider filling gaps in existing coverage by reviewing primary policies, insuring uninsured assets, and addressing employment-related liabilities.

By understanding the features, benefits, and importance of umbrella policies, you can better protect your assets and ensure a secure financial future.

Appendix: Frequently Asked Questions

1. What is an umbrella policy? + An umbrella policy is a type of liability insurance that supplements primary insurance policies. 2. How does an umbrella policy work? + Umbrella policies provide additional coverage beyond primary policy limits, protecting against catastrophic events and liability risks. 3. Why do I need an umbrella policy? + To safeguard your assets from liability risks, ensuring you have sufficient financial protection in the event of unexpected events.

Glossary

Liability insurance: Insurance designed to protect against claims made by others for injuries or property damage

Primary policies: Insurance policies that provide basic coverage limits and protection

Umbrella policy: A type of liability insurance that supplements primary policies, providing additional coverage and protection

This Article was made with AI assistance and human editing.